A few days ago, I decided to catch up with Tullow Ghana Ltd, a company some of us in the policy community keep an eye on because it is Ghana’s largest oil producer and the only company that has put any serious money in the country’s upstream petroleum sector in the last five or so years.

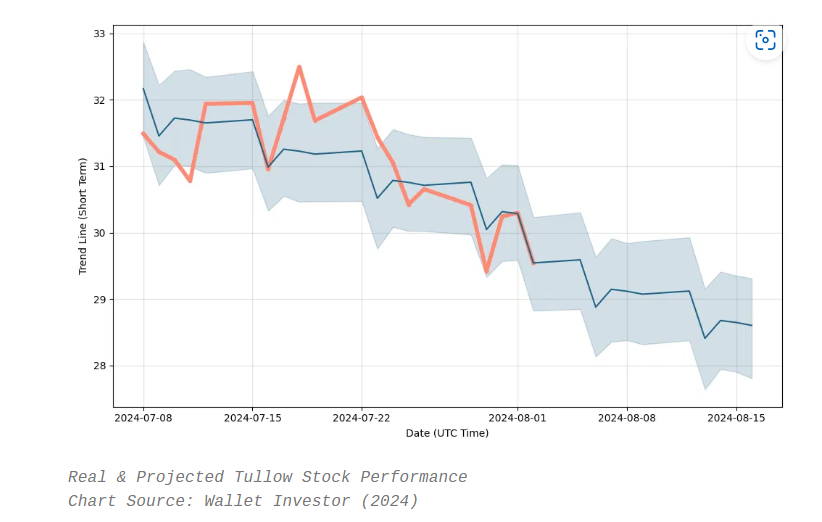

I saw that an upset in its plans to take forward its Lake Turkana project in Kenya has extended the lackluster performance of its share price on the London Stock Exchange.

I then thought to check the Ghana Stock Exchange (GSE), where Tullow debuted in 2011 with 0.45% of its outstanding shares valued about $73 million. When I checked, those same shares today would be worth about $2.7 million. Colossal erosion of value for long-term Ghanaian investors. More curious, though, is the fact that the share price hasn’t moved since 2018 and is locked at about 60 British pence despite the same stock now selling for less than 30 pence in London.

This random episode made me think about Ghana’s stock market in general, and how it is keeping faith with the country’s investor community.

The challenges that bedevil sub-Saharan African stock exchanges outside South Africa are well known. Low liquidity, low issuances, low subscriptions, low trading, low capitalisation…etc. etc. But there was a time when Ghana’s stock market was widely believed to be destined for greatness.

Great Expectations at the birth of GSE

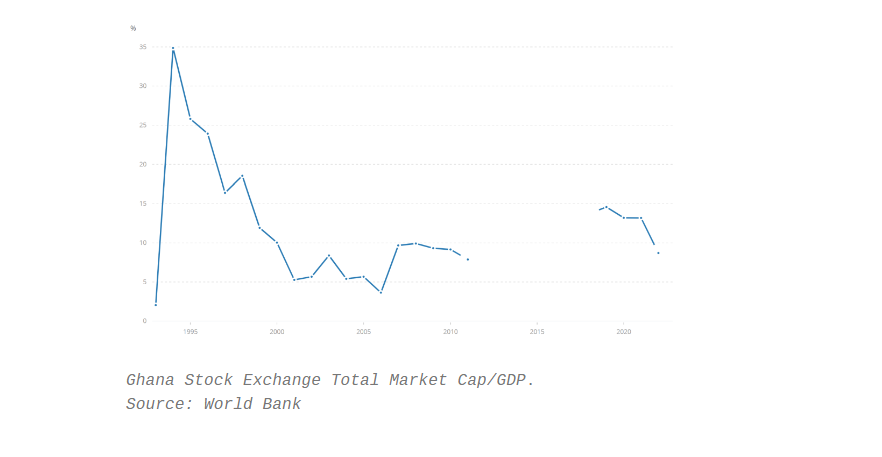

In 1994, four years after it was set up (in November 1990) with just 11 companies and a single corporate bond, its 124% annual index growth catapulted it to the attention of global analysts as the best “emerging stock market” in the world. The magical event that year was the listing of Ashanti Goldfields. Market capitalisation shot up to nearly 2 billion dollars, a grand 35% of GDP, 88% of which was contributed by Ashanti, heavily skewing average capitalisation per listed company to about $110 million.

Sadly, 1994 marked an early peak of the market. The likes of Ashanti Gold was never to be seen again.

As should be evident from the graph above, the market has seen some other short-run bull-charges, or limited periods of exciting performance, since 1994. A decade after the 1994 fiesta, the GSE was once more sprang to the front of the global queue of top performers. Year-on-year market capitalisation growth that year was an eye-popping 673%. Annual index growth was 91.32%. And total trading value hit 657 billion cedis.

A major trigger for this surge in activity was the record four Initial Public offerings (IPOs) of pharmaceutical pioneer, Starwin; spunky ICT innovator, Clydestone; CalBank; and Benso Oil Palm Plantation. On top of this, listed companies had successful rights issues, multiple investment schemes came to market, and Ashanti Gold closed its merger with AngloGold. Recall also that this was at the height of the whole “Golden Age of Business” giddiness. In fact, in that same 2004, Ghana hit the “floating completion point” of HIPC, after creditors provided “assurances” of debt relief confirming that Ghana was on course to meeting the terms of the program. Business confidence was booming.

That is not all, 1994 was also the year that Ghana’s first Central Securities Depositary was set up, simplifying the most critical aspects of trading shares on the market such as settlement, even though automation had still not been done, a whole 14 years after launch.

The last time the GSE would experience another miraculous run was also about a decade later, in 2013, just before the 2014 financial downturn. Index growth for that year nearly hit 80%. Once again, the trigger was a confluence of positive events.

A hard act to follow

Each truly spectacular change in market sentiment has, thus, been the product of several positive developments coming together. One might construe, therefore, that Ghana’s stock market only sees stellar performance on a “happy happenstance” basis, rather than on the back of durable secular trends.

Almost all the critical benchmark indicators like market capitalisation/GDP, turnover ratio (or the Hui-Heubel measure, a measure of liquidity), total value traded/GDP, etc. have all, from 2014 onwards, been on a downward slope, with a few punctuated moments of joy at long intervals.

There is no controversy in saying then that, since 2014, the performance of the GSE has been rather lackluster. For example, at the tail-end of the 2004 bull-run, market capitalisation was $10.8 billion. When I checked at the close of market last Friday, the equivalent number was $6 billion, less than 10% of current GDP (the global domestic average market cap is about 77% of GDP as of 2022). Adjusting by the number of listed equities, and US dollar inflation, the GSE’s market capitalisation today is at 1994 levels.

Ghana’s star dimmed a while back

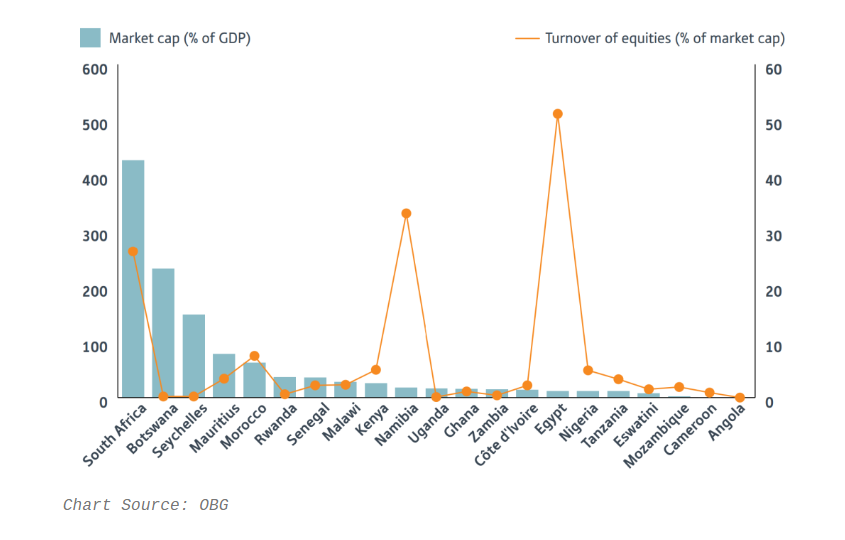

Even by African standards, Ghana’s current situation is not exciting. Between 1992 and 2018, African stock markets saw their capitalisation rise from $113 billion to nearly $1.15 trillion. Ghana could only achieve half of this growth rate. Today it sits at the top of the bottom half of regional rankings.

The low market cap is not helped by the fact that companies keep dropping off. The number of equities listed on the main exchange is now 31 (counting the two Stanchart equities as one), down from 37 in 2016. The shocking implication here is that since its founding, just one company enters the main exchange every two years.

There is of course a connection among turnover, market participation, and overall stock price sensitivity. After checking Tullow’s stock performance on Friday, I decided to take a peep at Atlantic Lithium, another company whose slow business strategy execution has lost it some market momentum in recent months. Whilst the stock is trading at just above 17 US cents in London, it is still stuck at 38 US cents in Accra, obviously due to the super thin trading volume. It seems that rather than a confluence of positive developments being on the horizon, mediocrity is cementing.

The early hopes of glory have simply not panned out. The GSE’s fate has been to join the mediocre ranks of sub-Saharan Africa’s struggling stock exchanges.

Any hopes for revival

What, really, can be done to spice up activity on the GSE? Get more companies listing, get more people trading, and see more share issuances, and eventually complex derivatives that will further drive liquidity and capitalisation growth?

Obviously, overall economic growth and improvements in business culture sophistication should help. As should macroeconomic rationalisation. When debt is returning at 30% to 60%, equities, usually considered more risky, must yield in the 100% range to be truly exciting. What kinds of businesses are going to be able to promise future growth at those levels to whet investor appetites?

But that cannot be all. Egypt has a larger economy than South Africa but as is evident from the graph above, South Africa is way ahead in terms of stock market activity. Tanzania, Zambia, and Kenya all have a more sophisticated economy than Malawi, but that little Southern African economy has often given them a run for their money. And Rwanda is clearly punching above its weight. These facts show lucidly that there could be factors endogenous to the capital markets that require further study.

It has not been for lack of trying, though

But let’s be fair, it is not as if the government of Ghana and the Ghana Stock Exchange aren’t aware of these challenges or haven’t made efforts to address them. In 2000, the government lowered corporate tax from 35% to 30% for GSE listed companies to attract more listings. That advantage has been wiped away by recent across the board drops in the rate of corporate tax, but it was there for quite a bit. Long before then, the government had granted tax exemptions on capital gains (profits made from trading on the stock exchange). That policy has been renewed in five year cycles until it was suspended during the “IMF return” period in 2015. The GSE is in active negotiations to make this a more longer-term affair.

Unlike is the case with the once popular fixed income market, foreigners are free to invest without strictures in stocks on the GSE (except in regulated industries where certain levels of ownership require prior approval). The government is also currently compelling companies in certain strategic sectors like mining to list a minimum of 20% of their outstanding shares on the Exchange.

In short, whilst there has been some inconsistencies in providing incentives, one cannot accuse successive governments of not caring about capital market development.

GSE Management does know what they are doing

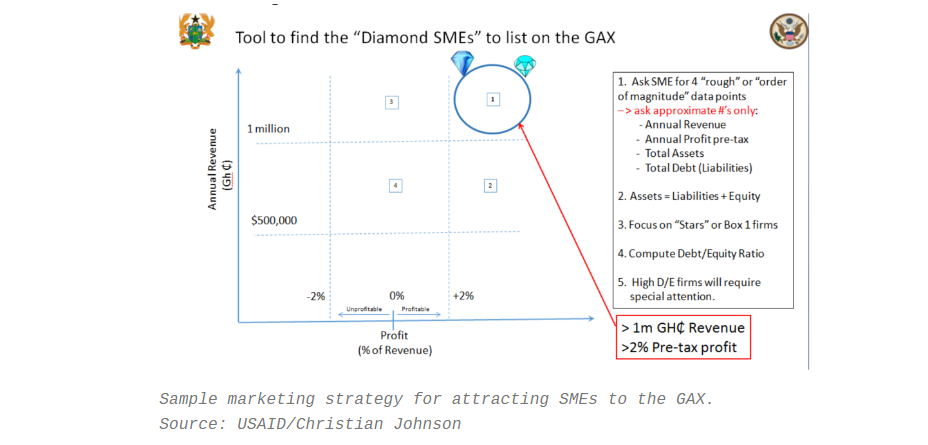

At the level of management, the GSE is now run by one of the most formidable corporate operators in the country, whose knowledge of the market and the formal corporate sector is virtually peerless. At last count, she has engaged dozens of interest groups and “stakeholders”, as we like to say in Ghana, to boost listings by small and medium businesses (SMEs) on the lower tier of the Exchange (known as the Ghana Alternative Market – GAX), moving beyond the original marketing strategy. MOUs have been signed to encourage groups and associations that interface with high-performing SMEs to consider listing on the GAX to benefit from the less stringent criteria and compliance burden, and of course the prospect of raising equity capital in an environment where interest rates for their segment regularly tops 40%. Despite all this effort, the number of GAX-listed companies have stubbornly stayed below 6 since the GAX’s creation in 2013.

Not to be deterred, the current management has launched a new regulated off-market trading platform for companies that do not wish to list at all, even on the GAX. Such trading is meant to boost liquidity in illiquid assets, whilst also giving prospective capital market actors a taste of the stock market.

The GSE has also jumped on all the fashionable bandwagons: green bonds, sustainability-linked indices, ESG, and ETFs, etc. Working in partnership with the World Bank’s private sector arm, the International Finance Corporation (IFC), it has launched a framework for issuance of these novel financial instruments in Ghana.

It is just a very hard nut to crack

My survey of the situation suggest that all these developments are failing to make a serious dent in the market apathy problem. Whilst the recent bull run (46.5% year-to-date composite index return) is being celebrated to the high heavens by the financial press, the truth, as outlined in previous passages, is that, judged in historical terms, there has been no progress at all. On a share of GDP basis, the GSE market cap growth level today is less than 30% of the performance in 1994, in 2004 (even on a rebased GDP basis) and in 2013. In absolute terms, the $6 billion market capitalisation figure being trumpeted today compares very unfavourably with the ~$30 billion attained over a decade ago.

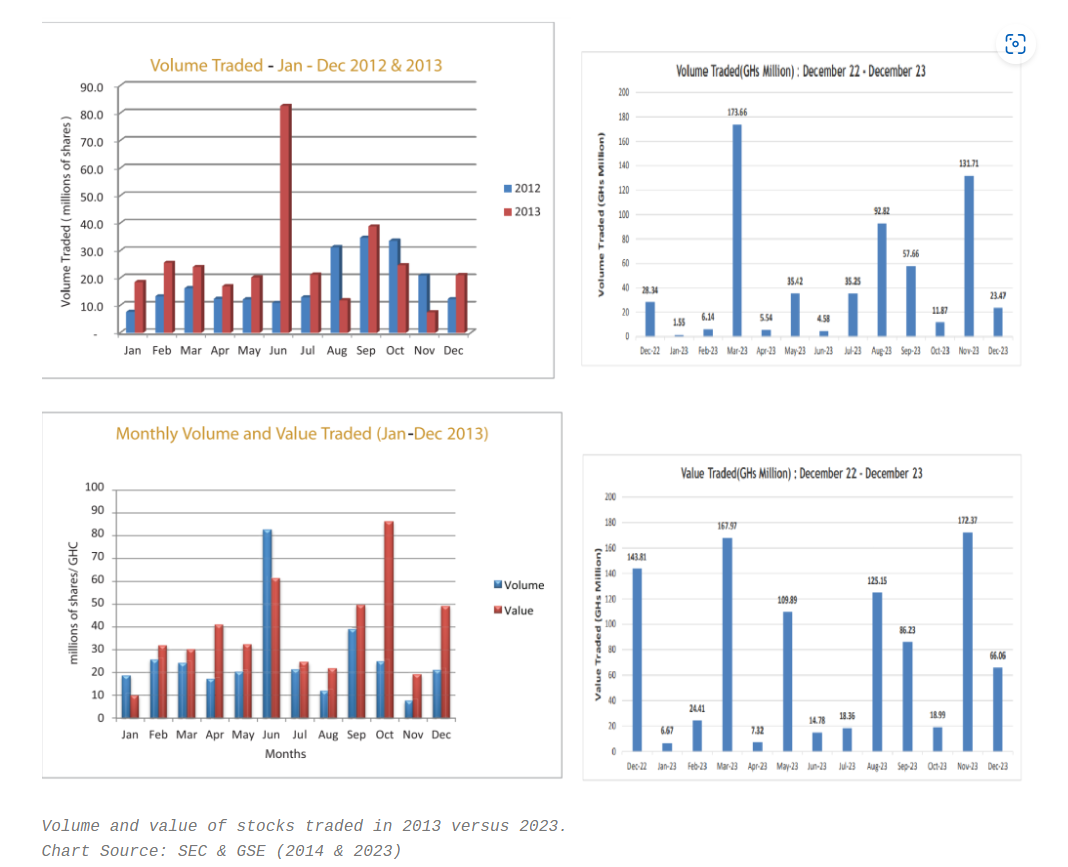

The results are similar if one compares the value of trading a decade ago to today’s. In 2013, total annual value traded was in the region of about $225 million. In 2023, the equivalent number was barely $72 million. Even using the best year by far of the decade, 2022, still yields a value traded figure of about $170 million, considerably lower than its historical peaks more than a decade prior.

The failure of equity markets in Ghana has had a devastating impact on the investment industry as a whole. The poor performance of mutual funds, unit trusts, and other collective investment schemes, including perennial liquidity challenges, has contributed in no small measure to the rampant distrust that has built up among financial consumers. The resultant overdependence of savers on fixed deposits at fantastic rates from the non-bank deposit taking players that resulted contributed to the massacre of the so-called “clean ups”. The country needs diversity of investment channels for savers to induce resilience in the financial system.

There may be a path, just maybe…

It is not hard to tell from how I have written about the subject so far that I do not accept the neo-Marxist claim that stock markets are a Western, neo-colonial, imposition on Africa. I have, however, began to wonder if the ideas of joint stock companies, split ownership, and share trading, and the high levels of disclosure required for all of these, sit well with our culture of doing business.

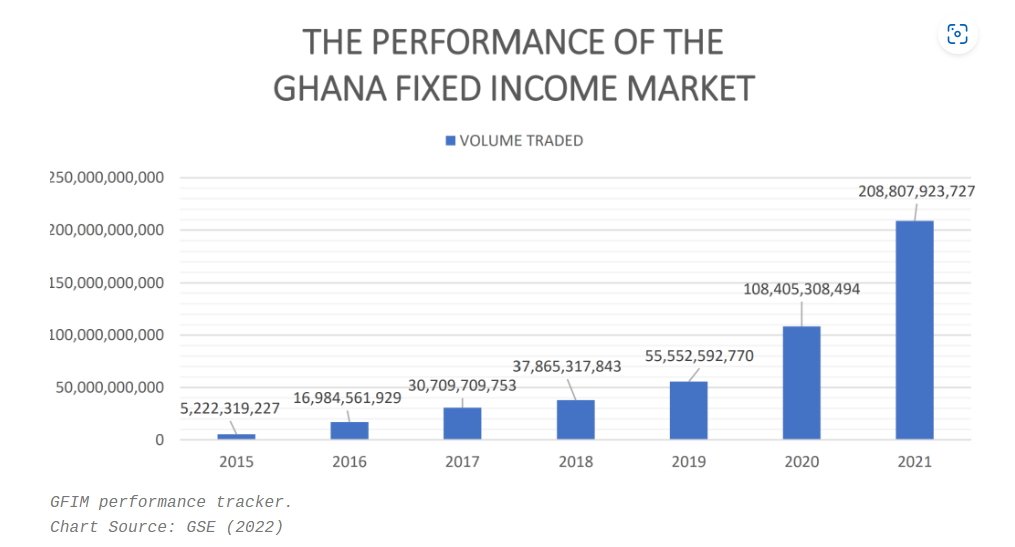

It is clear that until the recent domestic debt restructuring debacle, the Ghana Fixed Income Market was soaring with a consistency that must have been the envy of the equities players.

My intuition, fortified by limited research, is that debt is much more compatible with our capital infrastructure and business culture at this point in our economic development. The sophistication of transferability, securitisation, and other capital market techniques could probably be stretched further for the SME segment of the investment spectrum if the likes of the GSE were willing to get more creative with debt instruments than with equities. Unfortunately, the standard GFIM window at the GSE is much too stuffy for the SME sector.

It seems to me that rather than investing in the GAX as the primary strategy to create a high-throughput feeder and pipeline for the main index, the smart approach is to explore creative venture debt instruments targeted at SMEs in the new over-the-counter segment.

As a honey-trap to get the SMEs slowly acclimatised to the idea of listing, my sense, crude though it may be, is that this might be more seductive than share-listing, regardless of compliance burden. The marketing would, however, need to be way more camper than we have seen with the GAX. The right narratives, stripped of alienating jargon, and the right endorsement strategies would need to be explored for this to work. Much can be learnt from the halting steps to introduce crowd investment into Africa, which effort, unfortunately, has so far been stymied due to lack of institutional investor interest.

And, of course, cut and paste would simply not suit our environment, so engaging with the hubs and entrepreneurial networks that have sprawled all over Ghana and the near-abroad to get a deeper, anthropological, sense of what makes that whole ecosystem tick would be essential if a venture debt platform backed by the stock market and Ghana’s securities industry would have traction as a long-term booster of a more diversified capital market.

Explore the world of impactful news with CitiNewsroom on WhatsApp!

Click on the link to join the Citi Newsroom channel for curated, meaningful stories tailored just for YOU: https://whatsapp.com/channel/0029VaCYzPRAYlUPudDDe53x

No spam, just the stories that truly matter! #StayInformed #CitiNewsroom #CNRDigital

Read Full Story

Facebook

Twitter

Pinterest

Instagram

Google+

YouTube

LinkedIn

RSS