By Benjamin Nathan OTCHERE

As Ghana’s financial markets stabilise and Treasury bill yields settle into a lower trajectory, conservative investors face a crucial decision: remain with low returns or consider strategic options that combine safety with income and growth potential.

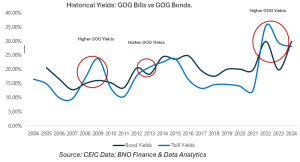

With Treasury bills now yielding between 10% to 13%(as of mid-August 2025) and government bonds offering 15% -17%, there is a timely opportunity to reassess your investment objectives and strategy. One viable option is a well-structured collective investment scheme (CIS), particularly a balanced fund, which can provide good returns while effectively managing risks for those concerned about the recent significant drop in GOG bills.

The balanced fund advantage

A Collective Investment Scheme (CIS), particularly balanced funds, represents a professionally managed investment vehicle that pools resources from multiple investors to create diversified portfolios. Unlike the singular focus of Treasury bills or government bonds, balanced funds strategically allocate capital across various asset classes, including equities, fixed income securities, money market instruments, and alternative investments.

The fundamental appeal of balanced funds lies in their dual mandate: capital preservation through conservative allocations combined with growth potential through strategic equity exposure. This approach directly addresses the primary concern of conservative investors who seek returns above inflation while maintaining reasonable risk parameters.

Strategic Diversification Matters and Benefits

While Treasury bills offer predictable returns, they expose investors to significant inflation risk and heighten concentration risk. With Ghana’s inflation rate at 12.1% as of July 2025, investors relying solely on Treasury bills, which yield 10-13%, face real returns that barely keep pace with the erosion of purchasing power. This scenario particularly affects pensioners, working-class individuals, and students who require their investments to maintain and grow their wealth over time.

Balanced funds mitigate this challenge through strategic diversification. By combining government securities for stability with carefully selected equities for growth, these funds can deliver inflation-beating returns while maintaining lower volatility than pure equity investments. The professional management component ensures that asset allocation adjustments occur based on market conditions, removing the burden of active decision-making from individual investors.

Current market performance: A compelling case study

Recent market performance data illustrates the significant opportunity cost of remaining exclusively in low-yielding government securities. To start with, the S&P 500 has delivered a 9.3%(in USD terms) return since January 1, 2025, demonstrating the continued strength of global equity markets despite various economic headwinds. This is more beneficial to those interested in having USD-denominated assets in their personal portfolio.

More relevant to Ghana-based investors, the GSE Composite Index surged 216.20 points to 6,992.29, marking about 43.03% year-to-date return as of July 2025. This exceptional performance highlights the potential rewards available to investors with appropriate equity exposure through professionally managed vehicles.

Additionally, alternative assets have shown remarkable resilience. Gold has been up over 24%(in USD terms) for the year, with specific gold ETFs like SPDR Gold Shares delivering a 26.97%(in USD terms) YTD total return, providing portfolio diversification benefits that pure government securities cannot offer.

As gold performs well in USD terms, the listed gold ETF on the GSE has underperformed at about -2.9%(as of 22nd August, 2025) because of the strength of the Ghanaian cedi. However, it will interest you to know that the mentioned ETF has done over 1000% in return from inception. So this is the time balanced fund managers are buying to get ready for the ride in the medium to long term.

Comparative YTD Performance Analysis (2025)

| Asset Class | YTD Returns(%) | Risk Profile |

| Ghana Treasury Bills | 10-13% | Very Low |

| Government of Ghana Bonds | 15-17% | Low |

| Bank Securities | 15-16% | Low |

| GSE Composite Index | 43.03% | High |

| S&P 500 Index | 9.30% | Moderate-High |

| New Gold ETF (GLD) | -2.94% | High |

| Typical Balanced Fund Range | 18-25% | Moderate |

This comparative analysis demonstrates how balanced funds, with their diversified approach, can potentially capture returns significantly above government securities while maintaining comparatively lower risk profiles than pure equity investments.

Why balanced funds suit conservative investors

For working professionals building retirement wealth, balanced funds offer systematic exposure to growth assets without requiring extensive market knowledge. The professional management component ensures that portfolio rebalancing occurs systematically, maintaining target allocations as market conditions evolve.

Pensioners benefit from balanced funds’ income-generating potential through dividend distributions and interest payments, while maintaining exposure to assets that can preserve purchasing power over time. The regular income distributions can supplement pension payments, providing financial flexibility during retirement years.

Students and young professionals gain a particular advantage from balanced funds’ long-term growth orientation. While maintaining conservative risk parameters appropriate for limited savings, these funds provide exposure to wealth-building assets that can compound over extended investment horizons.

The leverage: The professional management difference

Unlike individual stock picking or bond selection, balanced funds leverage professional portfolio management teams with specialized market expertise, research capabilities, and institutional-level access to investment opportunities. These teams continuously monitor economic indicators, assess market valuations, and adjust allocations to optimize risk-adjusted returns.

This professional oversight proves particularly valuable during market transitions, such as Ghana’s current dramatic normalisation period. Fund managers can tactically adjust allocations between government securities and growth assets based on evolving yield curves, inflation expectations, and equity market valuations.

Strategic considerations for balanced funds

Conservative investors considering balanced funds should evaluate several key factors. Fund expense ratios directly impact net returns, making cost-conscious selection important for long-term wealth building. Historical performance records, while not guaranteeing future results, provide insight into management team capabilities and fund consistency.

Asset allocation methodology represents another crucial consideration. Some balanced funds maintain static allocations, while others employ dynamic strategies that adjust based on market conditions. Understanding these approaches helps align fund selection with personal risk tolerance and return expectations.

Conclusion: Positioning for long-term success

Ghana’s evolving yield environment creates both challenges and opportunities for conservative investors. While Treasury bills continue offering predictable returns, their limited growth potential relative to inflation creates long-term wealth preservation concerns.

Balanced funds present a compelling alternative that addresses these concerns through professional diversification, strategic asset allocation, and growth-oriented investment approaches. The current market environment, characterized by strong equity performance and diverse investment opportunities, provides an ideal backdrop for conservative investors to enhance their return potential while maintaining appropriate risk parameters.

This piece is for educational and information purposes and should not be construed as financial, tax or investment advice. Read the CIS prospectus and seek professional financial advice before you invest.

Benjamin is a | Certified Financial Advisor & Planne

The post Beyond Treasury Bills: The CIS Opportunity appeared first on The Business & Financial Times.

Read Full Story

Facebook

Twitter

Pinterest

Instagram

Google+

YouTube

LinkedIn

RSS