By Raymond Denteh,

Introduction

Ghana once stood as a beacon of poultry self-sufficiency in West Africa. In the 1970s and 1980s, poultry farms across the country employed tens of thousands, while the industry supported a thriving ecosystem of maize and soya farmers, feed millers, veterinary suppliers, processors, transporters, and retailers. Chicken was fresh, local, and affordable.

This picture changed dramatically in the 1990s. Trade liberalisation dismantled the tariff protections that had safeguarded Ghanaian poultry producers. What followed was an onslaught of frozen poultry imports that the domestic sector could not withstand.

As cheap imports surged, farms closed, jobs disappeared, and maize and soya markets shrank. Today, Ghana consumes roughly 400,000 MT of poultry annually, but local production provides less than 60,000 MT. The gap is filled almost entirely by imports.

The EU’s Dominant Role

Among all Ghana’s trading partners, the European Union has had the most significant impact. After Russia banned EU poultry imports in 2014 and South Africa imposed restrictions in 2016 due to avian influenza, EU exporters redirected their surplus to West Africa. Ghana, with its liberalised market and rising demand, became a prime destination.

- Between 2014 and 2020, EU poultry exports to Ghana rose from 56,921 MT to 210,313 MT.

- In January–April 2025, EU exports to Ghana reached 59,474 MT, a 31.3% increase year-on-year.

- These exports often entered Ghana at $850 per tonne, far below the $1,600 per tonne cost of local production.

The result was devastating. Ghanaian farmers were forced out of the market, unable to compete against frozen poultry that was cheaper than producing a live bird domestically. The EU’s model of supporting domestic producers through tariff protections and then dumping unwanted cuts (such as wings, thighs, and backs) into Ghana is a textbook example of unfair trade.

Brazil’s Growing Influence

Brazil has long been one of the world’s largest poultry exporters. With vast production capacity, low feed costs, and economies of scale, Brazilian poultry companies have targeted Africa as an emerging market. For Ghana, Brazilian exports present two challenges:

- Price Competition: Brazilian poultry is among the cheapest globally, often undercutting EU prices. When EU export restrictions apply (such as during avian influenza bans), Brazilian exporters step in to fill the gap, further destabilising Ghana’s poultry sector.

- Market Substitution: If Ghana were to successfully restrict EU imports without a comprehensive trade framework, Brazilian poultry could easily replace them, leaving Ghanaian producers no better off. This substitution effect makes it essential for Ghana’s managed trade policy to cover all major suppliers, not just the EU.

Brazil’s efficiency rests on cheap maize and soya from its own agribusiness sector. For Ghana, this highlights the need to develop its domestic feed industry. If Ghana cannot produce affordable feed at scale, its farmers will never compete with Brazilian exporters who enjoy a built-in cost advantage.

The USA’s Impact

The United States is another major exporter of poultry meat, especially frozen chicken parts that are less in demand domestically. Like the EU, the US retains higher-value cuts for its home market and exports surplus parts cheaply to destinations like Ghana.

- US poultry exports to Ghana have grown steadily, particularly in the last decade.

- US exporters benefit from strong government support and subsidies that lower production costs.

The influx of US poultry has further reduced the viability of Ghana’s domestic farms. American exports also pose a regulatory challenge: their production systems are built on large-scale intensive farming models, often criticised for welfare and biosecurity issues. Ghana has little leverage to enforce standards, leaving it vulnerable to the dumping of low-cost, low-quality poultry.

China’s Emerging Role

China is a relatively new but increasingly important player in Ghana’s poultry trade. As the world’s largest consumer and producer of poultry, China has traditionally imported poultry only when domestic shortages arise. However, in recent years, Chinese companies have begun exploring African markets not only as buyers but also as potential investment destinations.

China’s impact on Ghana can take two forms:

- As an Exporter: China has occasionally redirected poultry to West Africa during oversupply periods. This adds another competitor to an already crowded import market.

- As an Investor: Chinese agribusiness firms have expressed interest in investing in poultry farms, feed mills, and processing plants in Ghana. While this could bring capital and technology, it also risks crowding out local investors if not carefully managed.

China’s growing presence therefore presents both opportunities and risks. Ghana must negotiate terms that ensure Chinese investments complement rather than dominate local value chains.

What this means—partner-by-partner

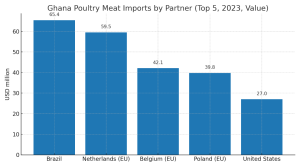

- EU: Still the principal source of Ghana’s poultry imports; 2025 YTD volumes show renewed growth. Persistent EU surplus parts (legs, back, thighs, wings) priced below Ghana’s local costs continue to crowd out domestic production. https://agriculture.ec.europa.eu/document/download/0ce25b9f-1571-4310-8531-3fe3346c49e0_en?filename=poultry-meat-dashboard_en.pdf

- Brazil: Cost-competitive and reliable supply; in 2023 it was Ghana’s #1 non-EU supplier by value and continues to feature prominently in 2024–2025 trade updates. https://www.media.mit.edu/projects/oec-new/overview/#:~:text=The Observatory of Economic Complexity (OEC) is the world’s leading,of millions of interactive visualizations.

- USA: Rapid recent expansion increases pressure on local producers, particularly in consumer-oriented segments (wings/parts). https://apps.fas.usda.gov/newgainapi/api/Report/DownloadReportByFileName?fileName=GHANA - Chicken Me Out - USA Poultry and Egg Export Council -USAPEEC- Stellar Training Program and Cooking Competition_Accra_Ghana_GH2025-0030.pdf&utm_source=chatgpt.com

- China: Currently minor in Ghana’s poultry import mix; no material market share in 2023 top partners and negligible volumes for whole birds. https://oec.world/en/profile/bilateral-product/poultry-meat/reporter/gha?utm_source=chatgpt.com

Internal Challenges and the Jobs Impact

While foreign competition has devastated Ghana’s poultry sector, internal weaknesses have also played a role. High feed costs (maize and soya), limited veterinary services, weak breeding and hatchery systems, and lack of affordable and appropriate finance all contribute to high production costs.

The employment impact has been severe:

- In 2000, the poultry sector supported around 120,000 jobs.

- By 2020, this had fallen to less than 15,000 jobs.

This decline has ripple effects. Feed millers have lost markets, maize and soya farmers face reduced demand, and ancillary industries—from transporters to processors—have shrunk.

Why a Comprehensive Managed Trade Policy is Essential

A managed trade policy is not about protectionism. It is about sequencing growth to allow domestic producers to compete fairly. For Ghana, this means:

- Negotiating Quotas: Engaging with the EU, USA, Brazil, and China to progressively reduce poultry export volumes to Ghana.

- Price Controls: Ensuring imports are not sold below the cost of production, which undermines local farmers.

- Gradual Transition: Recognising that Ghana will continue to need imports in the short to medium term, but ensuring these imports decline as domestic capacity grows.

- Feed Security: Expanding maize and soya production to reduce the single biggest cost in poultry farming.

- Attracting Investment: A predictable trade framework will give investors confidence to support breeding farms, hatcheries, production, processing plants, and integrated poultry ventures.

The Bigger Picture

If managed well, Ghana’s poultry revival will not only reduce dependence on imports but also strengthen food security, create jobs, and stimulate entire value chains. The maize and soya industries will benefit from reliable demand, while young entrepreneurs will have opportunities in farming, logistics, processing, and retail.

Recent studies show that broiler projects in Ghana remain financially viable with return-on-investments (ROIs) above 20% per cycle, even accounting for mortality rates. This demonstrates that the sector can thrive if imports are managed to create the necessary market space.

Conclusion

The poultry sector’s decline in Ghana is not inevitable—it is the result of policy choices, both domestic and international. A managed trade policy with the EU, USA, Brazil, and China is critical to reversing this decline.

Without it, Ghana will remain locked into dependency, with local producers permanently excluded from their own market. With it, Ghana can create a virtuous cycle of growth—protecting jobs, revitalising feed crop markets, and ensuring that the next generation of farmers and entrepreneurs see poultry as an opportunity rather than a graveyard of failed investments.

Reviving Ghana’s poultry sector requires courage, vision, and negotiation. The time for managed trade is now.

The post Reviving the poultry sector: A managed trade policy appeared first on The Business & Financial Times.

Read Full Story

Facebook

Twitter

Pinterest

Instagram

Google+

YouTube

LinkedIn

RSS