By Joshua Worlasi AMLANU & Ebenezer Chike Adjei NJOKU

Services, commerce and finance sectors accounted for the largest share of non-performing loans (NPLs) in the banking industry in 2024, underlining the persistent challenge of asset quality despite improvements in capital buffers and profitability across the sector.

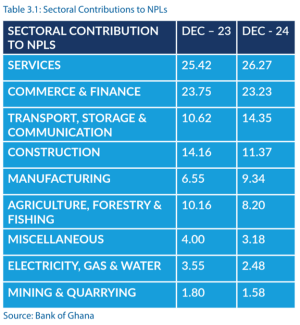

Together with the transport, storage and communication segment as well construction, the top four sectors contributed over 75 per cent of the industry’s impaired assets, according to the 2024 Financial Stability Review published by the Bank of Ghana (BoG).

The services sector alone accounted for 26.27 per cent of total NPLs, followed by commerce and finance (23.23 percent), transport, storage and communication (14.35 percent), and construction (11.37 percent).

Manufacturing and agriculture contributed 9.34 percent and 8.20 percent, respectively, with electricity, gas and water (2.48 percent) as well as mining (1.58 percent).

Interestingly all the sectors saw a decline in their share of NPLs except the services, transport and manufacturing spaces.

The banking sector’s overall NPL ratio deteriorated from 20.58 per cent in 2023 to 21.8 per cent in 2024, on account of the lagged impact of macroeconomic headwinds, including the effects of the 2022 Domestic Debt Exchange Programme (DDEP).

Despite this, the rate of migration from performing to non-performing loans slowed in the latter part of the year, ending at 8.1 per cent in December after peaking at 13.45 per cent in March 2024.

“These risks are expected to moderate on the back of recapitalisation, sustained macroeconomic recovery and enhanced risk management practices of banks,” the report read in part.

The BoG noted that, notwithstanding elevated default rates, banks’ ability to absorb credit losses improved. The ratio of NPLs net of provisions to capital—a key indicator of capital at risk—fell to 11.1 per cent from 14.6 per cent in 2023, suggesting enhanced provisioning and capital protection.

Overall, the banking sector maintained a sound financial footing as total assets rose by 33.8 percent to GH¢367.81 billion at end-December 2024, driven primarily by a 28.8 per cent growth in deposits, which continued to account for the majority of bank funding.

Household deposits, considered relatively stable, increased their share from 31.8 per cent to 35.8 per cent, while non-financial corporates contributed 56.42 per cent of total deposits.

The capital adequacy ratio (CAR) improved marginally to 14 percent, with Tier 1 CAR at 11.1 percent, both above regulatory thresholds. The leverage ratio remained broadly stable at 5.1 percent, exceeding the 4.5 per cent minimum requirement. These indicators were bolstered by regulatory forbearance, improved earnings performance, and a shift in asset allocation toward lower-risk investments.

Credit expansion was cautious as only 14.9 percent of newly mobilised funds were allocated to lending in 2024, although this was an improvement over 8.4 percent in 2023, in line with macroeconomic developments.

Notably, 62 percent of asset growth was directed towards cash and near-cash instruments, influenced by changes to the central bank’s Cash Reserve Ratio (CRR) requirements. These ratios, introduced in March 2024, varied based on banks’ loan-to-deposit ratios, ranging from 15 percent to 25 percent.

Profitability remained strong across the industry, aided by wider interest margins and improved cost efficiency. The cost-to-income ratio declined during the year, and non-interest expenses as a share of gross income continued to fall, reflecting better operating discipline. The apex bank noted that sustained profitability played a key role in maintaining solvency and supporting capital buffers.

Nonetheless, systemic interconnectedness continues to present stability risks. While banks’ direct exposure to other financial institutions remained modest at GH¢286 million, other sectors, especially securities and insurance firms, were significantly exposed to banks. Total exposure from non-bank financial institutions to banks rose to GH¢11.56 billion, with the securities industry accounting for GH¢5.9 billion, insurance – GH¢3.1 billion, and pensions – GH¢2.6 billion. This places the wider financial system at risk of contagion from stress in the banking sector.

In response, the BoG and the Financial Stability Council pursued various regulatory initiatives, including guidelines on large exposures, climate-related risk management, and enhanced credit risk supervision. These measures are expected to further strengthen risk governance and industry resilience.

At the close of the 125 Monetary Policy Committee (MPC) meeting, the BoG Governor, Dr. Johnson Pandit Asiama noted that the Bank is anticipating a modest recovery in credit expansion, supported by improving macroeconomic fundamentals, declining inflation, and greater business confidence.

“We have undertaken significant efforts to address the high level of non-performing loans. As I indicated in my statement, the NPL situation remains a matter of concern,” the Governor stated during the briefing.

“Our objective is not only to reduce the volume of NPLs, but also to strengthen the overall credit administration framework within the banking sector,” he further stated.

The post Services, commerce and finance top sectoral NPLs in 2024 appeared first on The Business & Financial Times.

Read Full Story

Facebook

Twitter

Pinterest

Instagram

Google+

YouTube

LinkedIn

RSS