By Ebenezer Chike Adjei NJOKU

The Ghana Stock Exchange’s (GSE) equity market is poised to extend its bullish run through the second quarter of 2025 as lower Treasury bill (T-bill) yields, a stable macroeconomic environment, and improved corporate earnings – particularly from the banking sector – continue to spur investor confidence.

This is according to Databank Research’s latest Ghana Market Quarterly Report for Q1 2025, which projects sustained market momentum anchored by favourable monetary dynamics and solid sector-specific fundamentals.

“Ghana’s equity market is expected to continue its rally through Q2-2025, buoyed by the ongoing macroeconomic recovery, upbeat investor sentiment and improved corporate earnings,” Databank stated in its report.

GSE’s Composite Index (GSE-CI) – which reflects overall market performance – is projected to reach 6,850 points by the end of 2025, translating to a return of between 40 percent and 50 percent.

“The stock market rally is expected to continue through Q2 ’25 on account of favourable corporate earnings amid recovery in economic activity. Given these positive backdrops, we reiterate our expectation of the GSE-CI closing around 6,850 points by the end of 2025 – translating to 45%±500bps,” a portion of the report read.

At the heart of the rally is a notable decline in yields on short-term government securities, which is prompting a reallocation of capital from fixed income to equities. T-bill yields, which reached highs of over 30 percent in 2023 amid inflationary pressures, are now projected to average between 15 and 16.5 percent in the second quarter of 2025.

This shift analysts have attributed to improving macroeconomic stability and renewed confidence in government’s fiscal consolidation efforts.

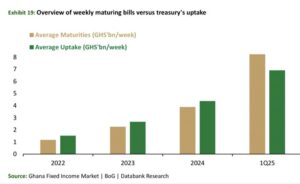

In first quarter of the year, yields on money market instruments hit 3-year lows with the 91-day bill dropping by 12.33 percentage points (pps) to 15.71 percent . Similarly, the 182-day bill recorded an 11.95pps decline to 16.73 percent while the 364-day bill settled at 18.65 percent, an 11.23pps decrease.

T-bill investor interest declined last week, with total bids decreasing by 27 percent week-over-week to GH¢5.29billion. The Treasury accepted GH¢4.73billion, which fell short of both the GH¢6.09billion in maturing bills and GH¢6.32billion target – resulting in coverage ratios of 0.77x and 0.74x respectively.

Yields decreased across all tenors, with the 91-day bill dropping by 9 basis points to 15.23 percent, 182-day bill falling by 26 basis points to 15.77 percent and 364-day bill decreasing significantly by 142 basis points week-over-week to 16.96 percent.

“The expected decline in yields on GoG local currency instruments is underpinned by improving investor sentiment and macroeconomic fundamentals,” the report stated, citing gradual easing of monetary policy and anticipated inflows from the International Monetary Fund (IMF) as contributing factors.

The nation is expected to receive a US$370million disbursement from the IMF in the second quarter under the ongoing Extended Credit Facility (ECF) programme.

Meanwhile, the banking sector has emerged as a key driver of stock market gains – registering a 29 percent increase in Q1 2025, the sector’s strongest quarterly performance in seven years.

The rally has been fuelled by robust earnings reports, renewed dividend payouts following regulatory clearance and improving asset quality as banks adapt to post-DDEP (Domestic Debt Exchange Programme) realities.

“The banking sector’s strong performance is attributable to earnings strength, resumed dividend payments and improved investor confidence,” Databank noted. The reinstatement of dividend payments, in particular, has re-energised retail and institutional investor participation on the bourse.

During the first quarter of 2025 GSE’s Composite Index (GSE-CI) concluded at 6,217.90 points, increasing from 4,888.53 points at beginning of the year – which represents a 27.2 percent gain. In a parallel trend the Financial Stocks Index (GSE-FSI) advanced from 2,380.79 to 3,059.30 points, delivering a 28.5 percent return over the same period.

Nonetheless, concerns remain over the industry’s relatively high non-performing loan ratios and low capital adequacy ratio. The former is currently at 21.8 percent and the latter at 14 percent.

Databank also highlighted a set of equities poised to outperform in the near-term, driven by company-specific and sectoral tailwinds. These include energy firm Total, which is expected to benefit from increased industrial and mining activity; Unilever, on account of operational improvements and renewed market strategy; Bopp, supported by strong crude palm oil (CPO) prices and consistent dividend policy; and Guinness, riding on price increases and strategic repositioning.

Guinness’s performance, in particular, reflects a broader trend of resilience among consumer-facing companies navigating currency depreciation and cost pressures.

“GGBL’s impressive 9M-2024 results, powered by price increases, indicate the earnings momentum will be sustained in 2025,” the report said.

The broader macroeconomic environment is also expected to remain supportive of equity market gains. Real Gross Domestic Growth (GDP) growth for Q1 2025 is estimated at 4.2 percent, up from 3.6 percent in the previous quarter with the second quarter forecasted to grow between 4.6 percent and 6.6 percent.

The services and industry sectors are projected to lead this expansion, despite some seasonal moderation in agriculture.

Monetary policy is expected to hold steady in the near-term, with the Bank of Ghana likely to maintain the policy rate at 28 percent barring any sharp inflationary surprises. The cedi is also expected to remain relatively stable, trading within a narrow band of between GH¢16 and GH¢16.2 to a U.S. dollar – supported by BoG interventions and the Gold for Reserves and Gold for Oil programmes.

“While market outlook is positive, the pace of yield compression may be tempered by still-elevated Open Market Operations (OMO) rates and the persistence of negative real returns,” the report cautioned. This highlights the need for continued policy discipline and structural reforms to maintain investor interest.

Global factors could also introduce volatility. Uncertainty stemming from geopolitical tensions, commodity price fluctuations and the evolving interest rate stance of major central bank – particularly the U.S. Federal Reserve – could influence market sentiment in emerging economies like Ghana.

Nonetheless, Databank remains confident in GSE’s performance trajectory for 2025. “We expect the market to continue its rally through Q2-2025 as the current macro backdrop, supported by fiscal consolidation and international financial assistance, remains broadly conducive to risk asset performance,” the report added.

The post GSE rally set to continue on back of lower T-bill yields, strong banking industry performance appeared first on The Business & Financial Times.

Read Full Story

Facebook

Twitter

Pinterest

Instagram

Google+

YouTube

LinkedIn

RSS