By Raymond DENTEH

Agriculture is Ghana’s heartbeat. It provides livelihoods for millions of families, feeds our communities, and contributes significantly to the national GDP.

From maize fields in the north to cocoa farms in the forest belt and vegetable gardens along river valleys, farming sustains our economy and culture.

Yet despite its central role, agriculture remains one of the most vulnerable sectors in the country. It is heavily exposed to climate extremes, market volatility, and systemic risks that often leave farmers, businesses, and consumers at the mercy of forces beyond their control.

The Harsh Reality of Drought

The 2024 drought was a painful reminder of how fragile Ghana’s agricultural base is. Spanning several months, the sun scorched crops across the country. More than 1.8 million hectares of farmland were affected, resulting in estimated losses of over GHS 22 billion between 2023 and 2024.

Staple foods were hardest hit: maize yields dropped by 35%, rice by 25%, and millet and sorghum by about 20%. Vegetable production collapsed except in small irrigated pockets near rivers and dams. Farmers watched helplessly as their investments withered, and households faced soaring food prices. Many families were forced to reduce meals or switch to less nutritious foods.

Thousands of farmers abandoned their fields altogether, migrating to urban centres in search of survival. This exodus further strained rural economies and reduced the agricultural labour available for the following season.

The 2024 Drought in Numbers

- 1.8 million hectares of farmland affected

- GHS 22.2 billion crop revenue lost (2023–2024)

- Yields dropped: Maize –35%, Rice –25%, Millet & Sorghum –20%

- Thousands of households displaced

The 2025 Dry Spell: A Warning That Risks Remain

If 2024 was a wake-up call, 2025 proves that the risks are far from over. A prolonged dry spell from mid-June to mid-August 2025 crippled grain production, especially in northern Ghana. Farmers reported delayed rains, erratic rainfall patterns, and wilting crops.

The USDA has already projected normal-to-below-normal rainfall with longer dry spells for the rest of the season, raising fears of another poor harvest. Livestock farmers have also been hit hard, with pastures drying up and animals losing weight.

Food prices, already elevated from the previous year, climbed further. Vulnerable households are feeling the squeeze most—spending more of their limited incomes on fewer, less nutritious meals.

The government has intervened by distributing seeds and fertilizer to 800,000 smallholder farmers, providing interest-free loans to commercial farms, and issuing food grants to distressed households. While these measures bring short-term relief, they are not enough to tackle the deeper problem: Ghana’s food systems remain dangerously exposed to climate risk.

The 2025 Dry Spell in Numbers

- Mid-June to mid-August 2025: prolonged dry spell

- Forecast: “normal-to-below-normal rainfall” and longer dry spells ahead

- Smallholder crops withering, livestock losing pasture

- Food prices rising, food insecurity deepening

- Government response: seed/fertilizer distribution, food grants, interest-free loans

Ripple Effects Across the Value Chain

When drought strikes, the impact cascades through the agricultural market system:

- Smallholder Farmers (SHFs): Lose crops, incomes, and food, while defaulting on loans.

- Outgrower Businesses (OBs): Struggle to source produce, undermining processing and exports.

- Financial Institutions (FIs): Face higher defaults and reduce credit to the sector.

- Input Dealers: Record falling demand for seeds, fertilizer, and services.

- Consumers: Pay higher prices for fewer, less nutritious foods.

The result is a vicious cycle where farmers cannot repay debts, agribusinesses cannot operate profitably, FIs withdraw credit, and consumers lose access to affordable food.

Why Risk and Resilience Matter

These crises underscore a hard truth: Ghana’s food systems are highly exposed. Every drought or dry spell sets off a national crisis. Without stronger risk management and resilience-building measures, each shock erodes livelihoods and undermines economic stability.

Yet the potential for transformation is enormous. Ghana has an estimated 1.9 million hectares of irrigable land, but less than 4% is developed. Expanding irrigation could protect crops from erratic rainfall, extend the growing season, and create new opportunities for dry-season horticulture. Combined with climate-smart agriculture—such as drought-tolerant seeds, soil fertility management, and agroforestry—the sector could become far more resilient.

Pathways to Resilience

Climate-Smart Agriculture (CSA): Drought-tolerant seeds, soil fertility management, and agroforestry.

- Irrigation Expansion: Unlocking Ghana’s 1.9 million hectares of irrigable land.

- Warehouse Receipt System (WRS): Enabling farmers to store grain, access credit, and sell later at better prices.

- Risk Products: Agricultural insurance—particularly parametric, weather-indexed solutions.

- Bundled Services: Linking inputs, credit, insurance, and markets into one package.

Crop Insurance as a Game-Changer

Among all resilience tools, crop insurance—and especially parametric weather-indexed insurance—stands out as transformative.

Unlike traditional indemnity insurance, parametric insurance does not require inspectors to verify losses. Instead, payouts are triggered automatically when weather indicators (like rainfall levels or drought) cross pre-agreed thresholds.

Why Parametric Insurance is the Best Fit for Ghana

- Speed: Payouts are immediate, enabling farmers to replant quickly or recover.

- Lower Costs: No costly field inspections make it scalable.

- Predictability: Clear rules build trust between farmers, insurers, and lenders.

- Encourages Investment: Financial Institutions (FIs) and agribusinesses lend more confidently when risks are hedged.

- Designed for Rain-Fed Systems: With over 80% of Ghanaian farmland rain-fed, parametric products fit the reality of smallholder agriculture.

Delivery Models for Ghana

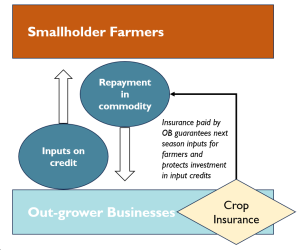

- Agribusiness-Driven Insurance

- Delivery Model – Premiums paid fully by the OBs/aggregators/other agribusinesses on behalf of smallholder farmers

- Premium will be paid by the OBs/aggregators/agribusinesses

- Claim payout – payout would be directly to the policy holder and they either give replacement inputs or cash to farmers for next season.

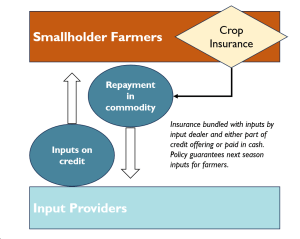

- Bundled with Input Sales

- Delivery Model – Premiums are to be paid by the SHF as part of the bundled input packages supplied by agribusinesses for payment in full or on credit.

- Insurance Premium will be paid by the smallholder farmers as a bundled cost of their input packages.

- Claim payout – Payments would be made to agribusinesses to re-supply inputs to SHF to replant.

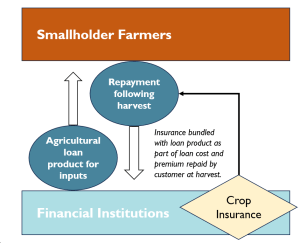

- Bundled with Agricultural Loans

- Delivery Model – Bundling insurance premium costs on commercially available agriculture credit products.

- Cost – Costs will be repaid to the FI by the producers after harvest. Cost of premium included as part of their loan package.

- Claims – Payouts cover loan balances with FI to refinance inputs to SHF to replant.

Each model protects farmers while reinforcing supply chains and credit systems. Together, they create a safety net that stabilises Ghana’s agriculture.

What Needs to Happen Next

- Scale up irrigation and dry-season farming.

- Embed parametric insurance in credit and input systems.

- Provide premium subsidies to lower adoption costs.

- Strengthen partnerships among insurers, FIs, agribusinesses, and farmer groups.

- Expand farmer education and awareness campaigns.

A Shared Responsibility

Resilience cannot rest on farmers alone. Policymakers must expand irrigation, incentivize private insurers, and regulate for fair coverage. FIs and agribusinesses must integrate insurance into input and credit packages. Farmer cooperatives must demand better protections. Development partners must support pilot schemes and premium subsidies to kick-start adoption.

Lessons from Beyond Ghana

Other countries offer lessons. Kenya and Ethiopia have rolled out large-scale parametric insurance programs linked to mobile payments, allowing payouts to reach farmers within days of drought triggers. India has integrated weather-based insurance into national farm subsidy programs. Ghana can adapt these lessons, building on its digital finance platforms and agribusiness networks.

Conclusion

The 2024 drought was a wake-up call. The 2025 dry spell proves the warning still stands. Without urgent action, Ghana risks repeating the cycle of loss and recovery every farming season.

Parametric insurance is not just a product—it is a lifeline. It delivers speed, transparency, and scale, giving farmers confidence to invest and lenders confidence to support them. Combined with irrigation expansion and climate-smart practices, it can transform Ghana’s agriculture from fragile to resilient.

Ghana has a choice: treat each drought as another crisis, or seize this moment to build a future-proof agricultural system that protects livelihoods, secures food supply, and drives economic growth.

The time to act is now.

The writer is an Agribusiness Enthusiast

The post Crops, climate and courage: The path to agricultural resilience appeared first on The Business & Financial Times.

Read Full Story

Facebook

Twitter

Pinterest

Instagram

Google+

YouTube

LinkedIn

RSS