By Joshua Worlasi AMLANU & Ebenezer Chike Adjei NJOKU

Credit enquiries in the financial sector more than doubled in 2024, driven by a surge in digital lending and greater use of credit data by financial institutions.

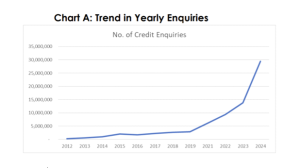

According to the Bank of Ghana’s (BoG) Credit Reporting Activity Report 2024, a total of 29.5 million credit searches were conducted by financial institutions and authorised users during the year; representing a 114.6 percent increase over the 13.7 million searches recorded in 2023.

This expansion was primarily driven by the growth in digital loans, which now account for nearly half of all searches. Of the total enquiries number, 44.4 percent (13.1 million) were linked to mobile-based or digital lending products; reflecting the rising use of mobile money platforms and app-based microcredit services across the country.

The report notes that the average number of credit searches per month stood at 2.46 million compared to 2.11 million in the previous year. Financial institutions, particularly deposit money banks (DMBs), dominated usage – accounting for 85 percent of all enquiries – followed by microfinance and microcredit institutions, which together made up 8.8 percent.

The sharp rise in credit enquiry activity highlights a broader transformation in the country’s credit market, driven by rapid digitisation and increased emphasis on data-driven lending.

“The increase in credit flows was mainly due to expansion of credit to the private sector,” the report noted, adding that this growth was “underpinned by a pickup in real sector activities” and improved transparency through credit referencing systems.

This rise in enquiries also corresponds with a 190.3 percent increase in the average number of monthly loan records submitted to credit bureaus, which reached 61.1 million in 2024. The report attributes this growth to improved digital loan data reporting, which now represents the bulk of individual borrower information in the licenced credit bureaus’ databases.

Credit referencing has become increasingly central to Ghana’s formal credit approval processes, with all licenced financial institutions required under the Credit Reporting Act, 2007 (Act 726) to conduct credit checks before approving or rejecting loan applications. The report confirms that 98.3 percent of all searches in 2024 were carried out specifically for credit application assessments.

Notably, the percentage of enquiries that returned usable credit data, known as ‘hit rates’, also improved. In 2024, 76 percent of searches resulted in hits – up from 72 percent in 2023; indicating both the growing depth of data coverage and improved data quality.

The report attributes this increasing hit rate to integration of digital loan records into credit bureau databases, making it more likely that borrowers have verifiable credit histories even at low-income levels.

“This is relevant, as a high level of hit searches is a measure of credit information depth in the credit bureaus’ databases and the credit reporting system’s integrity,” the report stated.

While digital lending has brought financial access to previously underserved populations, it has also introduced new complexities for lenders. Many of these loans are short-term and unsecured, increasing the importance of accurate borrower profiling. The report observes that individual borrowers accounted for 55.2 percent of all enquiries in 2024, underscoring the retail credit market’s continued expansion.

At the same time, corporate borrower enquiries fell sharply – from 472,579 in 2023 to 105,953 for 2024 – despite an overall 24 percent increase in gross credit to the private sector; suggesting that while nominal corporate lending may have risen, it is increasingly concentrated in fewer, possibly well-established firms, or that lenders are relying on alternative risk assessments for business clients.

The central bank has made it clear that credit referencing’s expansion is part of a broader strategy to deepen financial inclusion, reduce credit risk and encourage responsible lending. In 2024, it approved the implementation of credit scoring by licenced credit bureaus – a move expected to further streamline lending processes and expand credit access to underserved segments.

The Credit Reporting Activity Report notes that these developments have taken place alongside a slight rise in the non-performing loan (NPL) ratio, which increased to 21.79 percent for 2024 from 20.58 percent in 2023. The central bank believes that broader adoption of credit referencing and credit scoring will help lower this figure over time by reducing the risk of adverse selection.

Despite the strong growth in enquiries and data submissions, public participation remains limited. Self-enquiries – instances where individuals request their own credit reports – declined by 33 percent in 2024 to just 1,372; pointing to continued low levels of credit awareness among borrowers and highlighting the need for stronger consumer education.

The post Credit checks double on digital lending boom appeared first on The Business & Financial Times.

Read Full Story

Facebook

Twitter

Pinterest

Instagram

Google+

YouTube

LinkedIn

RSS