By Calleb OSEI (Dr)

Mobile money has transformed Ghana’s financial sector, becoming the preferred channel for payments and other financial transactions.

But as banks are increasingly integrating mobile money transactions into their operations, questions are emerging about how these are accounted for — and the risks that come with it.

Accounting for mobile money transactions within banks is a complex and evolving process. Although institutions may adopt different internal accounting approaches to reflect mobile money flows under the legal framework provided by the Payment Systems and Services Act, 2019 (Act 987), these practices must ultimately align with standard accounting principles to ensure transparency, fair reporting, and comparability.

My earlier publications (24 November 2021 and 11 April 2023) explored the evolution and progression of mobile money; its journey to market dominance in Ghana and the system mechanisms in terms of regulations and general guidelines for industry operations.

There was also an assessment of mobile money accounting with explanations based on various transactional scenarios involving banks and their customers.

This article extends the discussion, delving into key risk areas associated with Mobile Money Accounting and offering recommendations stakeholders can use to kick start the process of providing further guidelines to improve the overall reporting framework of mobile money transactions.

As in the case of all business processes, Mobile money operations carry inherent risks that if unaddressed, may derail the entire process, distort financial reporting and hinder effective regulatory oversight.

Three major risk areas are identified, assessed and possible remedial actions proposed to offset and/or mitigate their impact.

Perceived Artificial growth of Deposits and Total Assets

The key question is this: Is there a risk of artificial growth of deposits for banks that are involved in the mobile money value chain?

The answer: Possibly yes; under certain conditions.

To understand how deposits may appear to grow artificially, consider a simple trading business example.

Imagine a trader operating under different segments within the same business. If one segment sells goods to another, it will be reported as part of sales revenue by one segment and cost of purchases by the other.

However, in real business sense, and at the consolidated level, there will be zero impact on the Total Revenue and Assets of the business. As the goods remain in the business.

Segueing back to the business of Mobile Money, the same scenario plays out when Partner banks of Electronic Money Issuers (EMIs) purchase E –cash from the EMIs for their own use on the back of their Bank Identification Numbers (BINs).

There is no actual cash movement out as the account into which payment for the E-cash purchase is to be made, sits with the same bank.

Nevertheless, accounting entries are raised to show the purchase by Debiting (Dr) the internal account created for E-cash transactions and Crediting (Cr) the Trust Account of the EMI.

This results in simultaneous increase in the assets of the bank (other assets or cash and cash equivalent) by the value of the E-cash while total deposits (the Trust Account) also increases by the same amount. The process flow shown below presents in simplified terms the entries passed by the banks and their resultant impact on the bank’s books.

The regulator’s entries cancel out as they are a debit and credit to the same entity hence no cash movement. In this case both total assets and liabilities have been impacted even though actual or future cash movement is nil.

Unintentionally, a bank’s purchase of E-cash for its own use may lead to the creation of artificial deposits which impacts the balance sheet (total assets & total liabilities).

Partner banks, auditors and regulators may need to examine how “purchases for own use” transactions should be treated by banks as this may impact key industry data needed for proper planning especially liquidity management.

Recommendations

Regulators in examining the propensity of the scenario above happening and remedies to correct it may factor in the below recommendations as a means of mitigating the risk of artificial deposit creation.

Reporting Net Position of E-cash & Trust Accounts

As explained with the trader operating a segmental business, purchase of E-cash by Partner banks for its own use must have a nil impact on Assets and Liabilities.

Partner banks in reporting can net off the E-cash purchased for own use (which involves no actual cash movement) against the corresponding value in the trust account of the EMI whose E-cash they hold. By so doing, the risk of artificial deposit growth is completely eliminated.

Separate classification of E-Cash & Trust Account Balances

The commensurate deposit value for E-cash being held by the reporting bank in the trust accounts of EMIs should not be reported as part of the traditional deposits lines which include current/demand, savings or time deposits.

Instead, two separate deposit lines; Mobile Money Trust Account – Own Use and Mobile Money Trust Account – Others, should be created to record trust account balances that relates to E-cash of the partner bank (purchased for its own use) and trust account balances that relates to E-cash of other customers (whose bin is tagged to the partner bank).

The E-cash which the bank purchases for its own use should also be reported as a separate line item under other assets. This will allow for fair analysis by external parties. Regulators will also have firsthand information on actual total industry deposits to aid ratio computations for decision making.

Where trust account balances are included in any of the traditional deposit lines, partner banks will need to provide extensive disclosures in their annual accounts indicating which portion of the total e-cash and trust account deposits belong to the bank and which portion belongs to other customers (whose bin is tagged to the partner bank).

There should also be movement schedules as part of the notes showing changes to both the trust accounts and E-cash over the period.

Potential Misreporting of Income

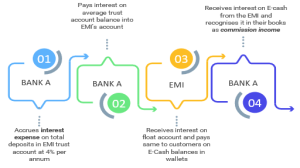

Partner banks of EMIs are required under Section 29(2) of the Payment Systems and Services Act 2019 (Act 987) to accrue interest on the total funds in the trust accounts of the EMI.

The EMI is then mandated to pay not less than 90% or as determined by Bank of Ghana, of these accrued interest less fees and charges to the electronic money holders whose funds are held in these trust accounts. Interest on these trust accounts is currently accrued at a rate of 4% per annum.

Partner banks that purchase E-cash for their own use per the above requirement are thus entitled to also receive a portion of the accrued interest on the trust accounts.

It should be emphasized that the 4% accrued interest is treated as normal cost of deposits and thus is disclosed as part of the Partner bank’s interest expense. Ideally, for proper reporting, the interest received by Partner bank on its portion of the trust account should be netted off against the interest expense booked for the entire trust account balance.

Where a partner bank decides to recognize the income received from the EMI on its e-cash as commission as opposed to netting off against interest expense; then the case of a perceived under/over statement of some income related lines visually represented in diagram below;

There is obviously a potential misreporting of income in the scenario above as the same bank pays interest expense on deposits from its e-cash and recognize same back as commission income.

Recommendations

To prevent the risk of misreporting income earned from e-cash held by partner banks for their own use, either of these two approaches should be adopted.

- Partner banks should not accrue interest on the portion of the EMI trust account deposit that relates to the E-cash purchased for the bank’s own use. By this the banks corresponding deposit for E-cash purchased for its own use would be separated from customer deposits and would not accrue any interest.

- Partner banks in reporting, should only recognize interest expense net of income received/receivable from EMI relating to its own E-cash.

Again, extensive disclosures should be included in the notes of accounts detailing how income is treated with regards to Mobile Money.

Distortion of Ratios

The way mobile money is treated on the books of banks has a significant impact on ratios considered key in the assessment of viability or otherwise of any business, especially financial institutions. Key among these ratios are Liquidity ratios, Return on Assets (RoA) and Capital Adequacy Ratio (CAR).

- Liquidity ratios

Where E-cash purchased for a bank’s own use is not netted off against deposits, it affects the bank’s liquidity ratio. As E-cash is reported under other assets, it is largely not considered a liquid asset for the purposes of computing liquidity ratio.

However, the trust account balance if is treated as part of deposit will include the balances relating to the e-cash purchased for the Partner bank’s use.

Thus total deposits which is the denominator will be unfairly increased and dampen the Partner bank’s liquidity ratio. By extension, the industry liquidity ratio can be impacted thus distorting the country’s data on the liquidity strength of its financial industry.

- Return on Assets (ROA)

Due to the supposed artificial growth in total assets, the return on assets ratio of partner banks may be misrepresented. Return on assets is an indicator of how profitable a company is relative to its assets and is computed by dividing a company’s net income by its total assets.

Bloated total assets will reduce the return on assets ratio and may give the indication that the company is not being as efficient in utilization of its assets as it actually is. Here again, the ripple effect of this misrepresentation would be felt by the industry as a whole.

This can partially be mitigated if the ROA is computed using operating assets, which will effectively exclude the e-cash balance included in the other asset line.

- Capital Adequacy Ratio

As currently pertains, per Bank of Ghana reporting guidelines, E-cash which is reported under other assets, is 100% risk weighted. Thus, even without any liquidity movements, this risk rating has an adverse effect on a partner bank’s Capital Adequacy Ratio.

Regulators should re-consider the risk weighting assigned to E-cash positions in the computation of capital adequacy ratio as in actuality, there are technically no risks with holding E-cash purchased for own use.

There are other impacts including operational cost from the angle of Deposit Insurance premium computation.

The Mobile money business has become a transformative force and a potential disrupter to the traditional banking systems.

Its integration into traditional banking however raises new accounting and regulatory challenges creating an urgent need to streamline reporting structures to ensure transactions are reflected appropriately on the books of partner banks and the EMIs as a whole and to ultimately safeguard transparency, comparability, and the accuracy of financial reporting systems.

The post Mobile money accounting 101 (Vol 3): Accounting for mobile money transactions: emerging risks, practical recommendations and the need for regulatory clarity. appeared first on The Business & Financial Times.

Read Full Story

Facebook

Twitter

Pinterest

Instagram

Google+

YouTube

LinkedIn

RSS