Background

As outlined in Section 28 of the Public Financial Management Act, 2016 (Act 921), the Finance Minister of Ghana delivered the Mid-Year Fiscal Policy Review for the 2025 Budget Statement and Economic Policy to Parliament on behalf of the President on Thursday, July 24, 2025.

The Centre for Economic Research and Policy Analysis provides key highlights and an independent perspective on the Minister’s presentation.

- Snapshot of Macroeconomic Indicators

Table 1: GDP & the Real Sector

| Indicator | 2024 Q1 | 2025 Q1 | 2025 target |

| Overall GDP Growth | 4.9% | 5.3% | At least 4.0% |

| Non-oil GDP | 4.3% | 6.8% | 4.8% |

Table 2: Fiscal Balance

| Indicator | Actual as of the End of June 2025 | Target at the End of June 2025 | Target at the End of December 2025 |

| Primary Balance on Commitment basis | 1.1% (Surplus) | 0.4% (Surplus) | 1.5% (Surplus) |

| Overall Fiscal Deficit on Commitment basis | 0.7%(Deficit) | 1.8%(Deficit) | 3.1% (Deficit) |

| Primary Balance on Cash basis | 0.7% (Surplus) | 0.2% (Deficit) | 0.5% (Surplus) |

| Overall Fiscal Deficit on Cash basis | 1.1%(Deficit) | 2.4%(Deficit) | 4.1% (Deficit) |

Table 3: Inflation and Interest Rates

| Indicator | End of December 2024 | End of June 2025 | |

| Interest Rates | 91-day T-Bill rate | 27.73% | 14.73% |

| 182-day T-Bill rate | 28.43% | 15.34% | |

| 364-day T-Bill rate | 29.95% | 15.76% | |

| Average Lending rate | 30.3% | 27.0% | |

| Ghana Reference rate | 29.31% | 24.0% | |

| Inflation | Consumer Price Inflation | 23.8% | 13.7% |

| Producer Price Inflation | 26.1% | 5.9% | |

| Food Inflation | 27.8% | 16.3% | |

| Non-Food Inflation | 20.3% | 11.4% | |

| Inflation for Locally Produced Goods & Services | 26.4% | 14% | |

| Inflation for Imported Item | 18.0% | 12.5% | |

| Gross International Reserves | 4 months of Imports | 4.8 months of Imports | |

Table 4: Exchange Rate Development

| Indicator | End of June 2024 | End of June 2025 |

| US Dollar | 18.6% Depreciation | 42.6% Appreciation |

| British Pound | 17.9% Depreciation | 30.3% Appreciation |

| Euro | 16.0% Depreciation | 25.6% Appreciation |

- Fiscal Performance

Table 5: Revenue and Expenditure

| Indicator | End of June 2025 (Actual) | June 2025 Target |

| Total Revenue and Grants | GH¢ 99.3 billion | GH¢ 102.6 billion |

| Non-Oil Tax Revenue | GH¢ 82.95 billion | GH¢ 82.2 billion |

| Non-Tax Revenue (non-oil) | GH¢ 8.0 billion | GH¢ 9.5 billion |

| Total Expenditure (Commitment, including discrepancy) | GH¢109.7 billion | GHS 128.0 billion |

| Expenditure on the Use of Goods and Services | GH¢1.9 billion | GHs 3.2 billion |

| Interest Payments | GH¢25.4 billion | GH¢30.5 billion |

| Capital Expenditure | GHs 7.1 billion | Ghs18.1 billion |

Table 6: Revision to the 2025 Revenue and Expenditure Targets

| Indicator | 2025 Budget Target | Revision of 2025 Budget Target |

| Total Revenue and Grants | GH¢ 227.1 billion | GH¢ 229.9 billion |

| Total Expenditure (Commitment) | GH¢ 270.9 billion | GH¢ 269.5 billion |

| Interest Payments | GH¢ 64.1 billion | GH¢ 59.9 billion |

| Primary Expenditure | GH¢ 206.8 billion | GH¢ 209.6 billion |

| Overall Fiscal Deficit on Commitment basis | 3.1% (Deficit) | 2.8% (Deficit) |

| Overall Fiscal Deficit on Cash basis | 4.1% (Deficit) | 3.8% (Deficit) |

Total revenue and grants amounted to GH¢99.3 billion by the end of June 2025, falling short of the target of GH¢102.6 billion.

Total spending was significantly lower than intended, amounting to GH¢109.7 billion compared to the target of GH¢128.0 billion, primarily due to shortfalls in capital expenditures (GH¢7.1 billion actual versus GH¢18.1 billion target) and interest payments (GH¢25.4 billion against a target of GH¢30.5 billion).

While the reduced interest burden offers temporary fiscal relief, the sharp drop in capital expenditure raises concerns about the government’s ability to execute development projects, with potential implications for growth and job creation.

The government has revised upward its total revenue and grants target for the year to GH¢229.9 billion, alongside a modest reduction in expenditure to GH¢269.5 billion. These revisions improve the fiscal deficit projections from 3.1% to 2.8% on a commitment basis and from 4.1% to 3.8% on a cash basis.

The downward revision of interest payments by GH¢4.2 billion suggests possible gains from restructuring or more favorable borrowing terms.

Our View

Although the mid-year data indicate stronger-than-anticipated domestic revenue outcomes and some fiscal discipline, shortfalls in essential sectors such as capital expenditure and non-tax revenue necessitate immediate policy adjustments. The task moving forward is to secure revenue improvements while better managing the budget, with a focus on investments that drive growth. A stronger focus on public financial management, project implementation capacity, and accountability will be vital in the second half of 2025.

- Public Debt and Debt Restructuring Programme

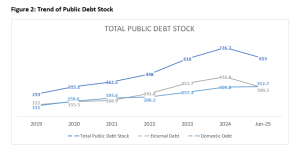

Figure 2: Trend of Public Debt Stock

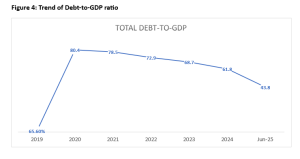

Figure 4: Trend of Debt-to-GDP ratio

At the end of June 2025, the public debt had decreased to GH¢613 billion, down from GH¢726.7 billion at the end of December 2024, indicating a reduction of GH¢113.7 billion within six months.

This progress has also positively impacted Ghana’s debt-to-GDP ratio, which declined sharply from 61.8% at the end of 2024 to 43.8% by mid-2025.

Our View

The decline in public debt and the debt-to-GDP ratio indicates a positive outlook for debt sustainability. This has been a result of appreciation of the cedi, lower domestic borrowing and the external debt restructuring. However, the extent to which this improvement is driven by exchange rate depreciation warrants closer scrutiny. The key question is: can this trend be sustained if the cedi begins to depreciate again?

Also, there is a need for the government to clearly define an exit strategy from the debt restructuring programme (DRP) and how it will ensure it does not plunge back into higher debt levels. When will the restructuring phase be considered complete? What will the post-DRP debt management policy look like?

- Update on key policy initiatives

- The Ghana Gold Board

In the first half of 2025, the reforms implemented by the Ghana Gold Board (GOLDBOD) governing the local gold trading sector have already produced tangible economic benefits.

- Gold exports from the small-scale mining sector of 51.5 tonnes valued at approximately US$5 billion exceeded gold exports from the large-scale mining sector.

- The substantial foreign exchange inflows from the GOLDBOD’s operations in the artisanal small-scale mining sector have significantly strengthened Ghana’s gold reserves, reduced reliance on foreign currencies, and improved the country’s balance of payments.

- The strong gold reserves have helped to stabilise the local currency and enhance exchange rate management.

Our View

- To enhance the value of exported gold, the government could promote or mandate local refining of raw gold to increase its value before export.

- The government can partner with local private investors to produce gold jewels for export.

- 24-hour economy

The policy document of the program has been launched by the President. It is now awaiting parliament’s deliberations.

Our View

- The government must first invest in an effective communication network, sustainable power solutions, effective security measures, and transportation systems, because delays or inefficiencies in these projects could hinder the development of the 24-hour economy.

- There is a need for a periodic, robust monitoring and evaluation system.

Ghana Medical Trust Fund (MahamaCares)

The Ghana Medical Trust Fund bill has been launched, and the bill has been passed by parliament.

Our View

- The bill was laid before Parliament without the mandatory fiscal impact analysis as required by Section 100 of the Public Financial Management Act. This omission undermines transparency and prevents lawmakers from fully evaluating the Fund’s sustainability and implications for the national budget.

- The proposal to allocate 20% of National Health Insurance Fund (NHIF) resources to the new Fund risks weakening the financial capacity of the National Health Insurance Authority (NHIA). This diversion could hamper the NHIA’s ability to deliver essential healthcare services unless compensatory measures are clearly outlined.

One Million Coders Initiative

The Ghana-India Kofi Annan Centre of Excellence in ICT (GI-KACE) has developed 30 specialised training courses in data analysis, cybersecurity, and networking to equip participants with globally relevant digital skills. The One Million Coders initiative, which was launched in April, has successfully trained 859 young participants during its pilot phase.

- GI-KACE in ICT has provided digital skills training at foundation, intermediate and advanced levels to 1,603 persons.

- For girls in ICT, Ghana Investment Fund for Electronic Communications (GIFEC) empowered 1,000 girls in the Volta Region with hands-on training in coding and web design.

- Looking ahead, a One Million Coders Programme is set up to meet the 100,000 target.

- Four new courses in Deep Learning AI, IoT, and Cybersecurity will be introduced to keep pace with global trends.

Our View

- Such large-scale investments have the potential to boost economic development; however, their success depends on effective funding strategies, efficient implementation, and sustainability.

National Investment Bank (NIB) Recapitalization

- The minister announced the recapitalisation of the government-owned bank, which was in distress.

- So far, GH¢450 million cash has been injected, GH¢1.5 billion bonds issued, and GH¢500 million shares in Nestle Ghana transferred to NIB. The bank’s Capital Adequacy Ratio (CAR) improved from -53.13% to 23%.

- There are also plans in place for listing NIB on GSE and ensuring sustainability.

Our View

- Government’s decision to “spend to save” rather than collapse NIB reflects a pragmatic financial sector posture.

- However, there is a need to ensure that NIB goes back to its core function of funding large investment and development projects and not just focus on retail banking as any other bank.

- Conclusion

- The 2025 Mid-Year Fiscal Policy Review reflects Ghana’s cautious but encouraging progress towards fiscal consolidation and macroeconomic stability. Amid the backdrop of IMF-supported reforms, the government has demonstrated commitment to restoring investor confidence through improved revenue mobilization, restrained expenditure, and decisive debt restructuring efforts. The significant reduction in public debt, improved primary balance, declining inflation, and strong currency performance are commendable outcomes that suggest a return to prudent economic management.

- To maintain this momentum, it will take more than just short-term gains. There are still important questions regarding the durability of the fiscal surplus, the sustainability of public debt after restructuring, and the ability to finance new policy initiatives without turning to unsustainable borrowing. Key initiatives such as the Ghana Gold Board, the 24-hour economy, the Ghana Medical Trust Fund and the One Million Coders Programme hold promise; their long-term impact depends heavily on effective execution, adequate financing, and institutional accountability.

- As the country navigates the second half of the fiscal year, the government must focus on consolidating gains, clearly defining exit strategies from temporary relief measures, and strengthening resilience against future shocks. Ghana cannot achieve long-term growth and shared prosperity unless it sustains discipline, structural reforms, and implements inclusive policies.

The post Highlights of the Mid-Year Budget review and CERPA’s view appeared first on The Business & Financial Times.

Read Full Story

Facebook

Twitter

Pinterest

Instagram

Google+

YouTube

LinkedIn

RSS